The year in numbers

Much of the last 12 months may have felt like an annus horriblis, but the industry also demonstrated its resilience…

No matter which sector of the superyacht industry you work in, you will be relishing the opportunity to down tools, take stock over the festive period and look forward to a more positive year ahead.

We have all lived and worked through a catastrophe not of our own making, and only the most bullish individuals could claim they have not found this year to be the most challenging in our industry’s history.

While economic crashes can, arguably, be managed, a global pandemic gives little warning and even less scope for strategic planning in its wake. It is a testament therefore that, despite fairly torrid operating conditions, the superyacht industry enters 2021 with much reason to be positive.

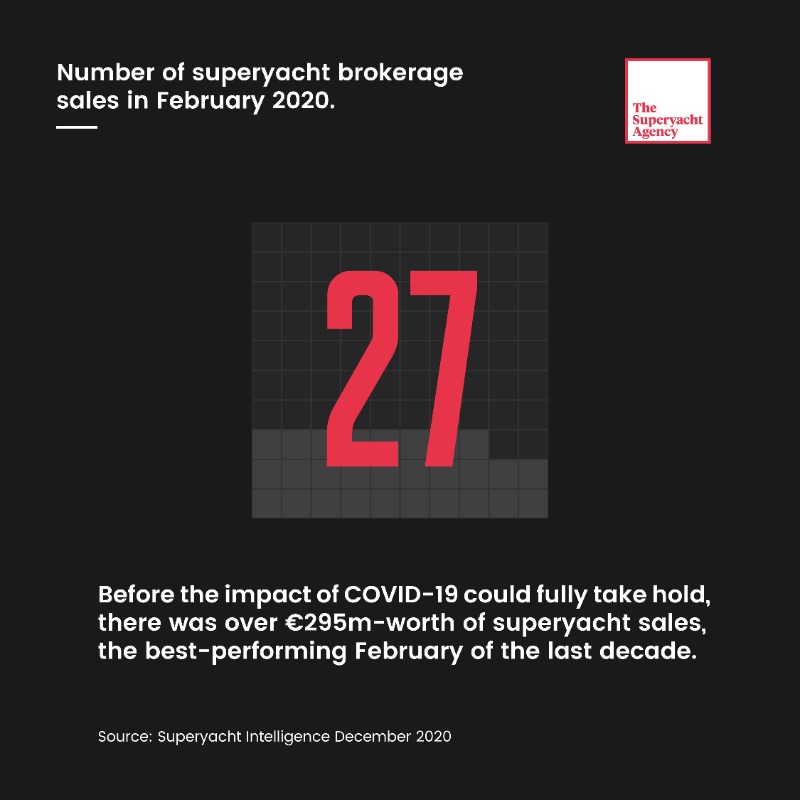

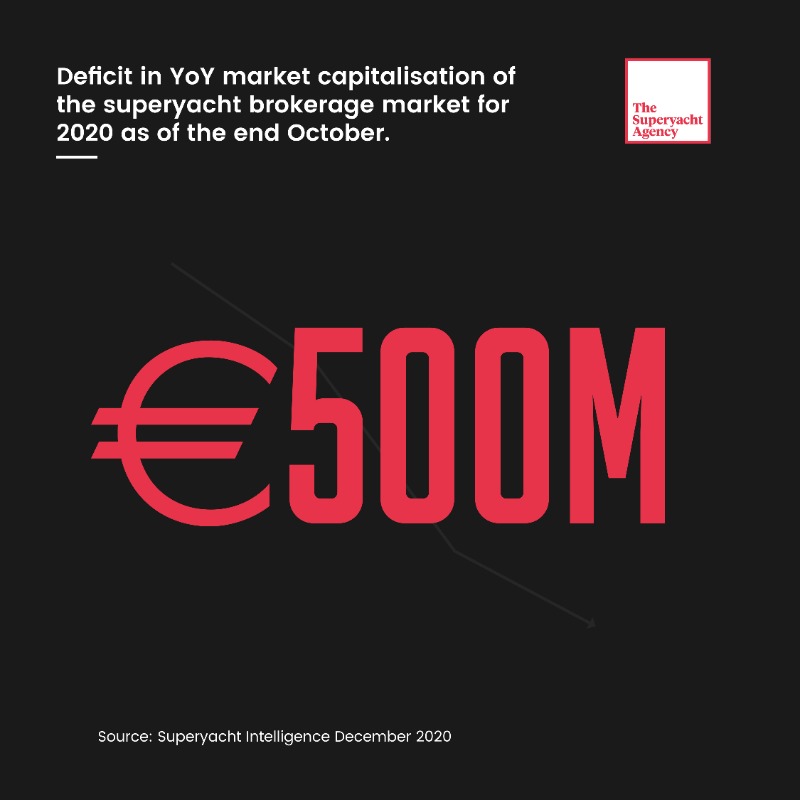

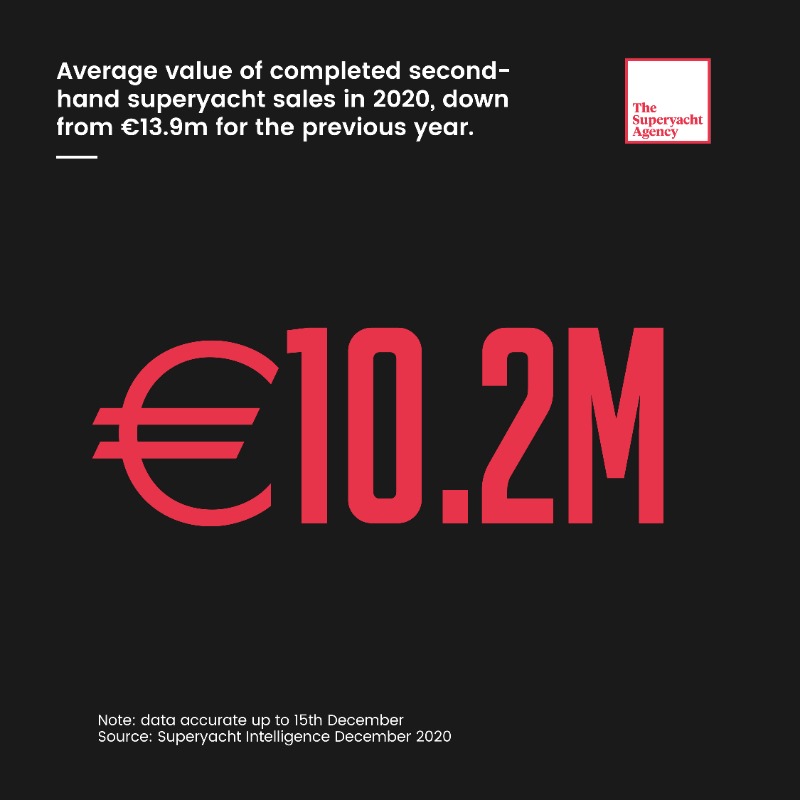

Indeed, before the West had fully acknowledged or understood the gravity of what was happening in China, the market seemed one of resplendence. In February, a month before the lockdown rules spread across Europe, the brokerage market had recorded its single most prolific February in a decade, with €295m of sales.

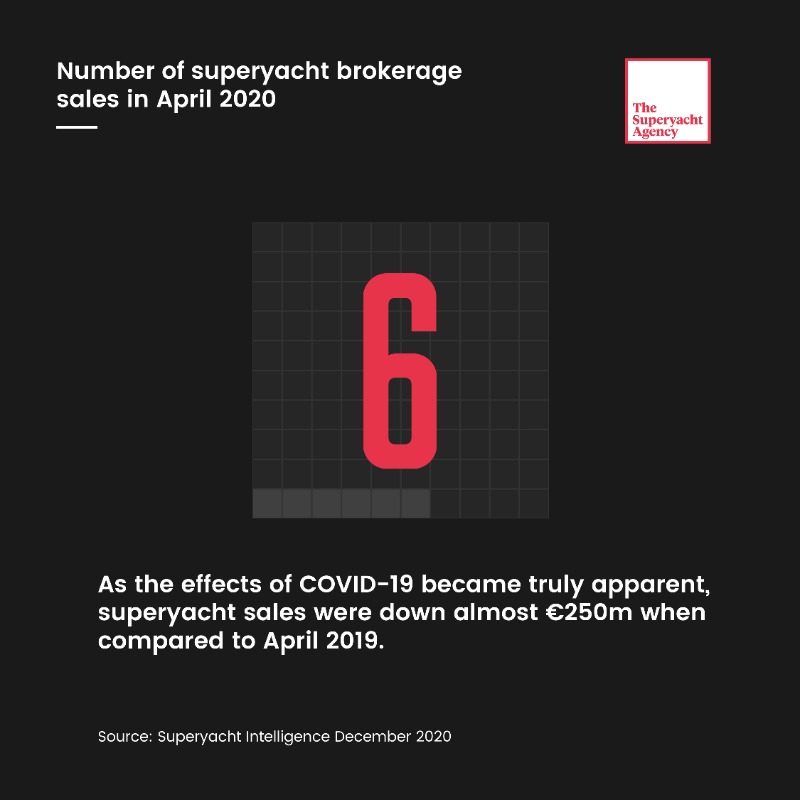

However, by April, and with the world fully in the grips of a pandemic, the impact on yachting was evident. The precocious February figures had made way for just six second-hand sales globally in April, €250m down YoY.

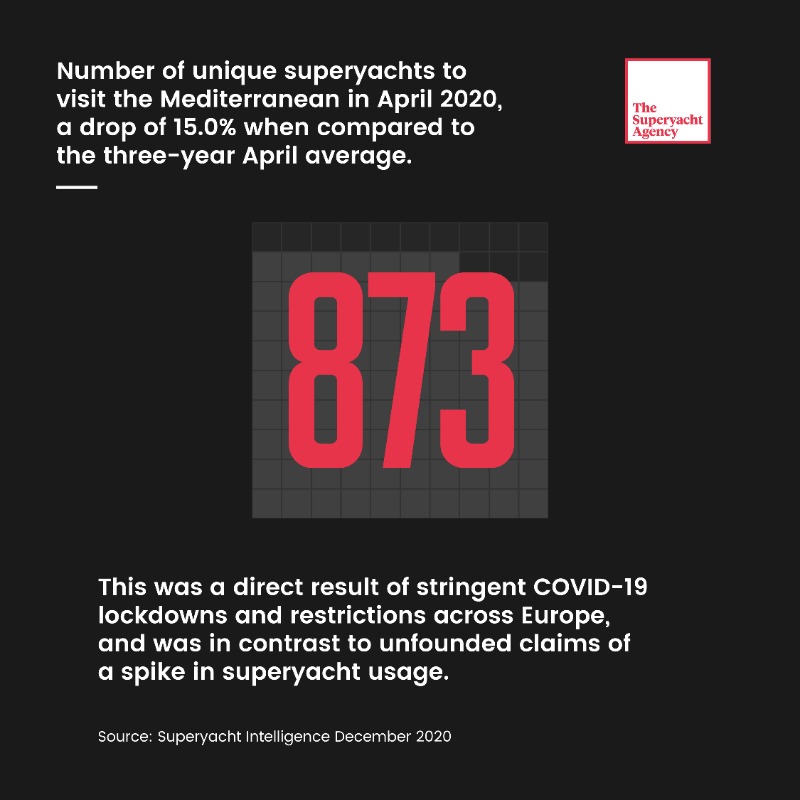

Despite much fanfare, and formulaic journalism based on anecdotes and hyperbole that suggested superyachts had become part of a mass exodus of the wealthy to the world’s oceans, activity in the Mediterranean in April 2020 was down 15.0% on the previous three-year average.

But as previously mentioned, our industry is nothing if not resilient, and although there is still much work to do in our collective path to stability and prosperity, the numbers have begun to show signs of improvement.

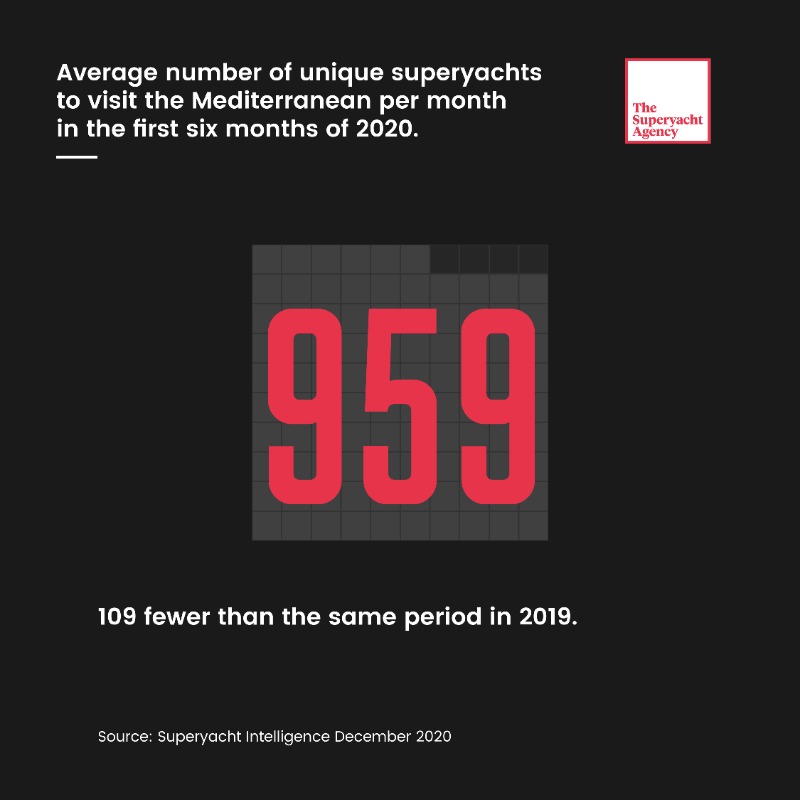

By August, there were signs of recovery and a return of confidence; Mediterranean superyacht activity for example, was just 10.2% down YoY.

There also remains a significant backlog of inventory, both in the new-build order book and the refit market, that will require work, and serves as a stimulus for the industry as a whole.

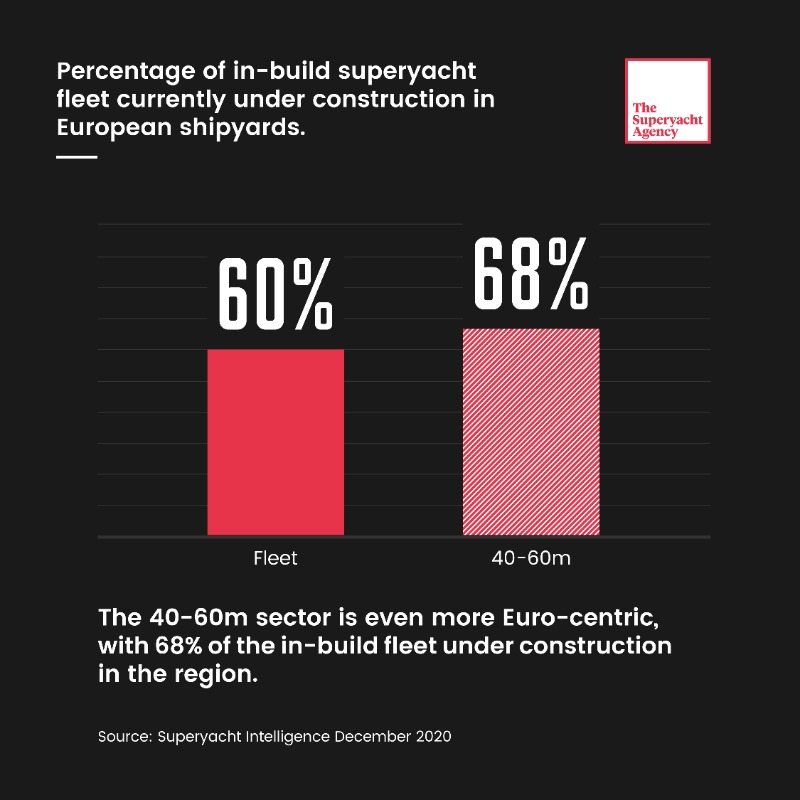

The number of shipyards with a project due for delivery within five years has risen YoY, pointing to a more active and competitive market. Although Europe has tightened its stranglehold on construction, with 60% of all vessels in build, in European yards, rising to 68% between 40m and 60m.

And a particularly profound statistic to conclude this piece of reflection, and one perhaps for all of us to take stock of, as it encompasses the trickle-down economics we’re all beholden to; at the time of writing, the cumulative value of the superyacht fleet due for delivery in the next five years is €14.3 billion. Cause for optimism indeed!

The Superyacht New Build Report is the first issue of 2021, and represents the return of The Superyacht Group’s annual industry-leading audit of the new-build market. To subscribe, click here.

Our consultancy division consistently provides clear and cogent narratives to businesses in every sector of the industry, as well as investors and their advisory teams externally. If you would like to separate the truth from anecdotal fiction, and require intelligence to support your 2021 strategic planning, please contact the Superyacht Intelligence team.

NEW: Sign up for SuperyachtNewsweek!

Get the latest weekly news, in-depth reports, intelligence, and strategic insights, delivered directly from The Superyacht Group's editors and market analysts.

Stay at the forefront of the superyacht industry with SuperyachtNewsweek

Click here to become part of The Superyacht Group community, and join us in our mission to make this industry accessible to all, and prosperous for the long-term. We are offering access to the superyacht industry’s most comprehensive and longstanding archive of business-critical information, as well as a comprehensive, real-time superyacht fleet database, for just £10 per month, because we are One Industry with One Mission. Sign up here.

Related news

Data is king

How the intelligent gathering and use of data can improve the client experience

Business

Partnerships, sustainability and well-being

YPI's director, Abdullah Nahar, discusses business development post-acquisition and working life during the pandemic

Business

SeaNet sells fourth co-owned superyacht

SeaNet announces the sale of MY UNY, a 35m Benetti Mediterraneo for six like-minded owners

Owner

One to One: Barin Cardenas

The founder and CEO of Yacht Creators offers a unique insight into the state of the US sales market

Business

A buyer’s guide to the 30-50m sailing yacht segment

This sector in decline still has a variety of options for the prudent buyer

Fleet

The Buyer Journey: Buying a second-hand yacht

The brokerage market is rife with nuance and, therefore, due diligence and expert advice are essential

Owner

Related news

Data is king

6 years ago

Partnerships, sustainability and well-being

6 years ago

SeaNet sells fourth co-owned superyacht

6 years ago

One to One: Barin Cardenas

6 years ago

The Buyer Journey: Buying a second-hand yacht

6 years ago

A buyer’s guide to the 70-90m motoryacht segment

6 years ago

A buyer’s guide to the 60-70m motoryacht segment

6 years ago

The Buyer Journey: The importance of class

6 years ago

A buyer’s guide to the 50-60m motoryacht segment

6 years ago

NEW: Sign up for

SuperyachtNewsweek!

Get the latest weekly news, in-depth reports, intelligence, and strategic insights, delivered directly from The Superyacht Group's editors and market analysts.

Stay at the forefront of the superyacht industry with SuperyachtNewsweek