What is the future of ownership?

Martin H. Redmayne quantifies the potential for new ownership based on the number of individuals who could afford to enter the market…

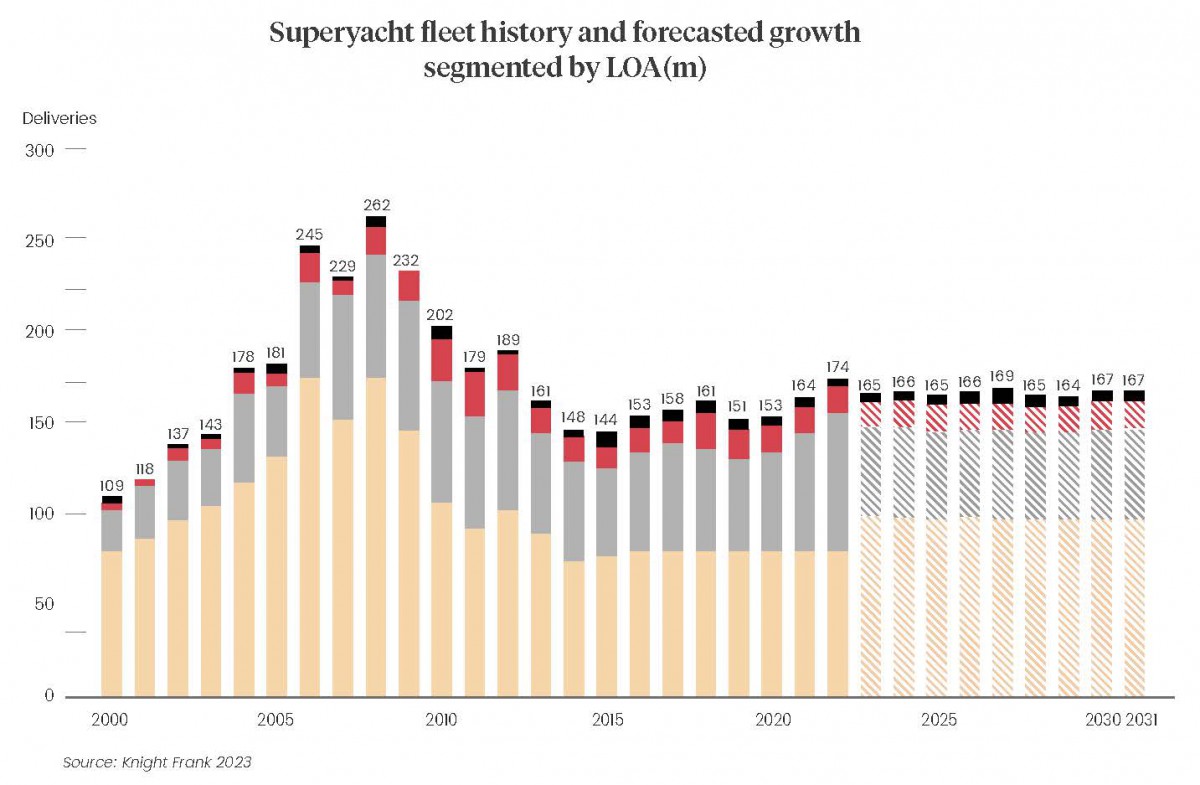

Over the past decade, we’ve dedicated a significant amount of time to modelling and forecasting our industry. When we take the current market scope and size into consideration, we’re currently building approximately 160 superyachts annually, ranging from 30m to more than 150m. Many of these are intended for existing experienced owners, while some are actively for sale, built on speculation, and others cater to first-time buyers who are starting their journey with various sizes of new constructions.

With a superyacht fleet comprising more than 5,500 yachts measuring over 30m – of which 25 per cent were built before 1990 – we quickly realise that the modern market, developed over the past 30 years, consists of around 4,500 yachts, including those set to be delivered in 2023 and 2024.

We estimate that this fleet is owned by approximately 3,700-plus individuals if one takes into account owners who possess two or more superyachts. Essentially, the market is primarily supported by a small group of passionate individuals who consistently invest in the superyacht lifestyle.

When reviewing the age and demographic of experienced owners who have undertaken new projects throughout their lives, we find ourselves entering a phase where mortality becomes a factor. In recent years, we’ve witnessed the passing of well-known and respected owners, along with their expertise and passion. Simultaneously, a new generation of owners has entered the market, becoming captivated by the process. They build serial projects, expanding their personal fleets to include two, three or more new projects or second-hand upgrades.

This trend suggests new owners are gradually replacing old ones as they fully immerse themselves in our unique industry. However, this raises a critical question when we delve deeper into the numbers: What does the future of ownership hold?

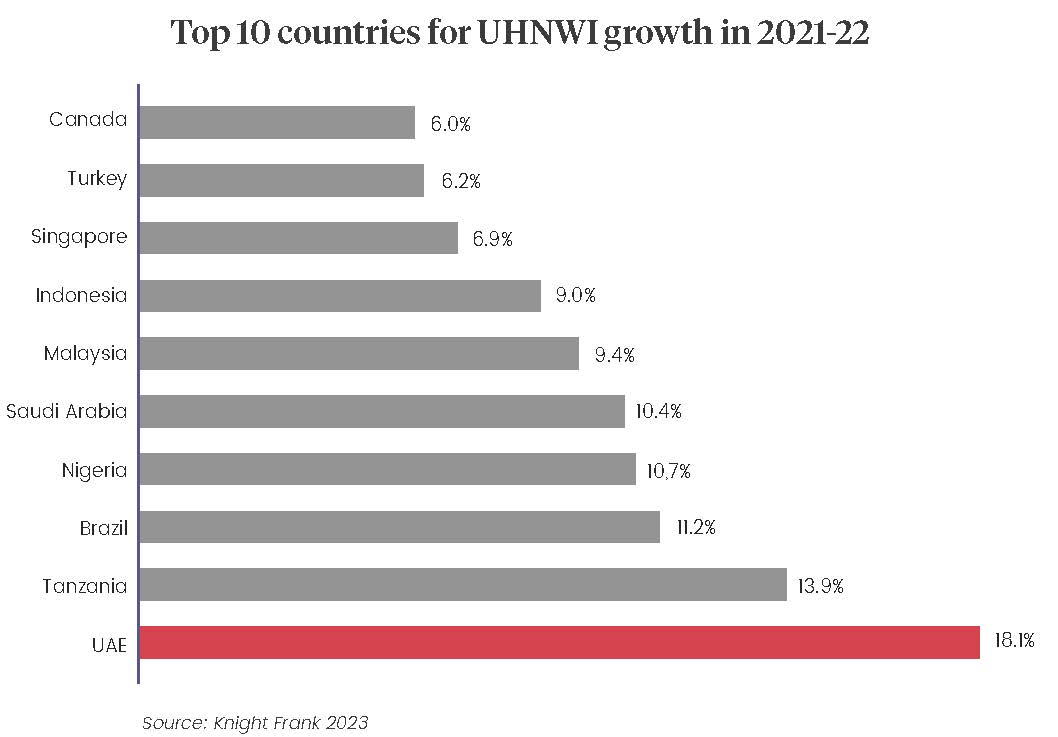

The statistics provided here, along with the charts embedded in this report, demonstrate the current growth and long-term potential of our industry based on the patterns and behaviour of our typical customer base.

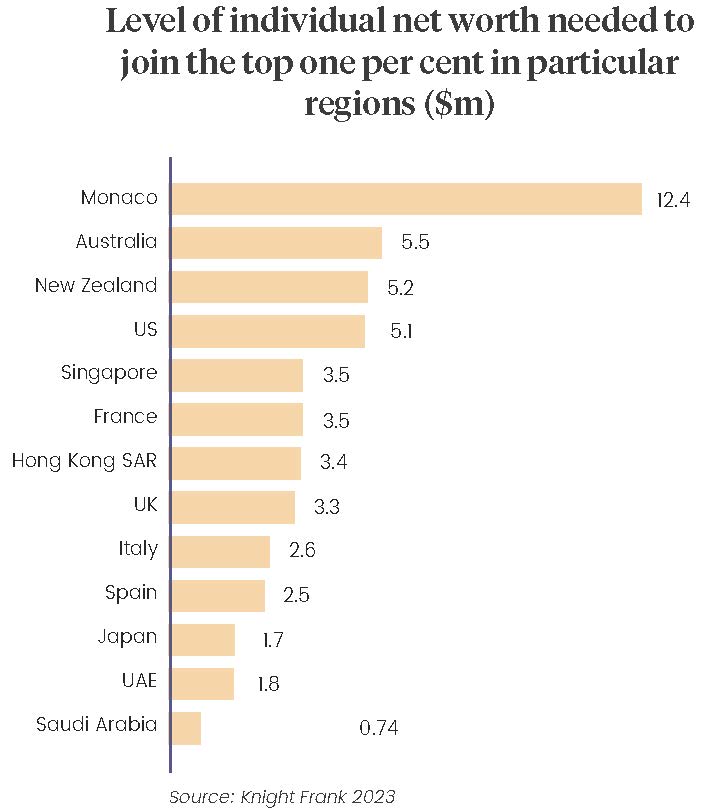

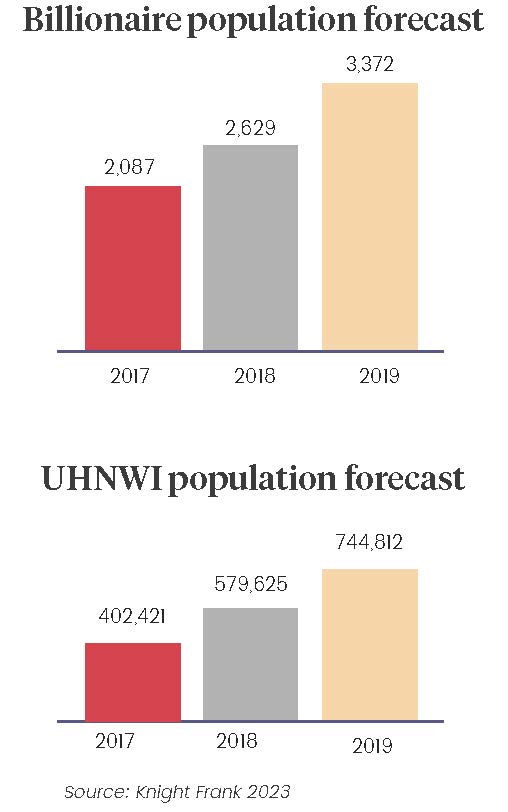

However, as we explore the real potential and consider the number of UHNWIs with the wealth and capability to enter our market (current estimates place this figure at 450,000 worldwide), we must pose additional questions such as ‘Are we content with the current growth trajectories?’, ‘Why aren’t more people buying yachts?’ and ‘Could there be alternative opportunities for our industry?’

Let’s attempt to answer these questions …

Are we satisfied with the current growth trajectories?

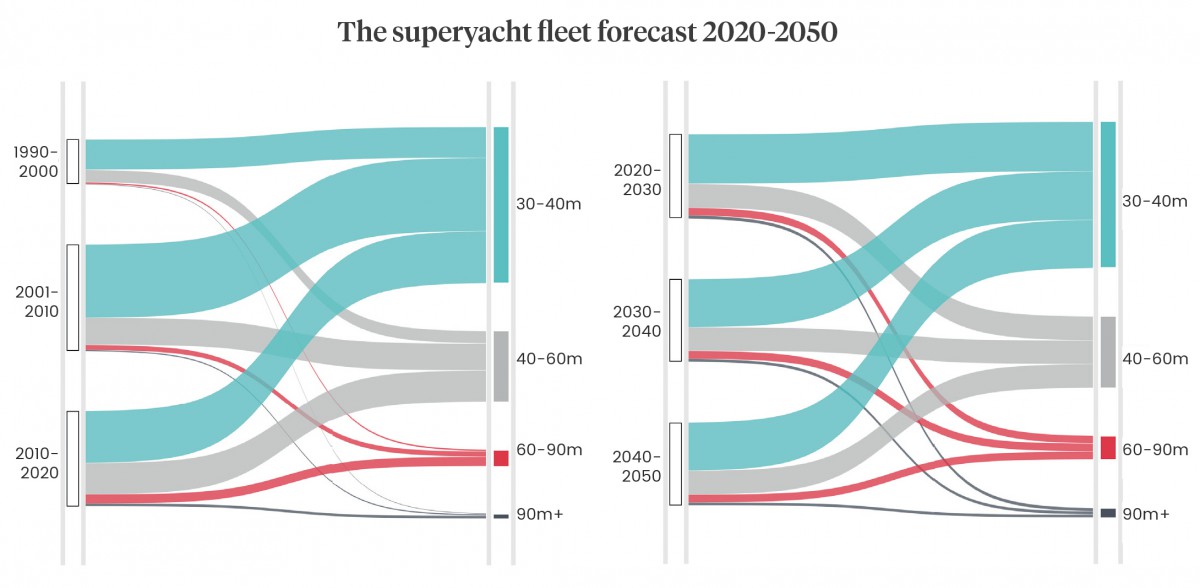

If we continue on our current course and deliver according to the existing order book, the market will enjoy a healthy future. Some stakeholders prefer maintaining the status quo and are content with the current state of affairs. Analysing market behaviour and growth curves, by 2030 and even further into 2050, our fleet is projected to expand significantly.

As project sizes and scopes increase, technology and innovation drive the next generation of ventures, and labour and raw-material costs rise in line with market forces and geopolitical factors, it’s foreseeable that not only will our market expand, but its value and revenues will also increase.

However, although clients continue to invest in new assets and enjoy constructing novel and exciting ventures, the rising costs of new builds and capacity constraints raise questions about whether this trajectory is sustainable. After all, we do create some of the most expensive toys, assets and floating real estate on the planet.

If our current new-build capacity is approximately more than 160 new superyachts per annum, and if we need to find several hundred buyers each year to secure their build slots across over 40 primary shipyards, with investments ranging from €20 million to €250 million, it may seem like a straightforward task when considering the potential market. But we need to add a few caveats to the question.

The term ‘we’ doesn’t solely refer to the industry, shipyards or advisors; buyers, owners and investors must also be considered. Are they content with the growth curve? This is a question we’re starting to focus on because we need to ensure that current and future customers are willing to continue investing in our niche and perhaps explore ways to transform it into a more serious industry for the future.

Superyachts represent a significant expense with minimal financial returns or asset appreciation ... a tipping point may be reached that challenges the status quo and potentially alters our growth curves.

The more investable and stable our industry becomes, the more owners and fellow UHNWIs might perceive it as an intriguing opportunity. As previously highlighted, superyachts represent a significant expense with minimal financial returns or asset appreciation. Furthermore, when considering the time spent on board compared to the investment and operational costs, a tipping point may be reached that challenges the status quo and potentially alters our growth curves.

If we add into the equation the next generation of yachts featuring alternative fuels, sustainability and green innovation, we must ask how relevant our industry will be in the coming decade and how much these factors will impact our market’s trajectory. We’re concerned that as we transition to the next phase of our industry and encounter an increasing number of rules, regulations and barriers, some clients, and certainly future clients, might conclude that ownership isn’t the most rational approach.

Why aren’t more people purchasing yachts?

Various opinions, theories and principles have been explored to answer this question. Put simply, we remain a relatively young industry, and during the Covid period we gained heightened visibility as some of the safest, most private and secure forms of real estate on the planet. Consequently, we witnessed an influx of first-time buyers into the market. Nevertheless, this is a modest increase when compared to the true potential.

So we must consider this question and delve into the actual answers. The reasons why there are not more first-time buyers range from simple constraints such as insufficient time to fully enjoy or explore the market, capital intensiveness, some family members not enjoying sea travel and even horror stories or unfavourable experiences shared by acquaintances who own yachts.

However, it’s more likely that those who can afford to buy choose not to due to limited exposure to our niche. The current market trajectory appears satisfactory, as is evident from order books, charter bookings and transaction announcements. The market seems to be in relatively good health, but this has led certain sectors to become complacent, no longer actively cultivating and nurturing new customers given the flow of new inquiries.

Is there an alternative opportunity for our industry?

In exploring opportunities, we must also acknowledge potential threats. This matter will be discussed in depth at The Superyacht Forum in Amsterdam in November. Currently, our industry faces high-profile attacks from non-governmental organisations (NGOs) or protest groups that campaign against ‘the haves and have-nots’, highlighting the potential environmental impact that superyachts might generate.

The issue of wealth inequality and societal pressure is gaining momentum. Despite some in the industry ignoring these concerns and asserting that superyachts have a notably positive impact, it’s important to acknowledge that negative rhetoric and climate-related criticisms are likely to increase.

Superyachts, due to their visibility and extended periods spent in ports awaiting travel instructions, are susceptible targets. Consequently, we can anticipate escalating threats to our industry, regardless of our efforts to embrace green practices and alternative fuels. As we encounter more rules, regulations and barriers, certain clients, particularly the next generation, might conclude that superyacht ownership is not the most viable option.

All these considerations beg the question: Is there an alternative opportunity and, if so, what does it entail? As we recognise, we construct some of the most intricate and complex toys worldwide. However, given the nature of our clientele, time spent on board is typically limited to days or weeks, with some yachts only actively hosting guests for less than 10 weeks per year.

Today, no one makes money out of owning a superyacht and they generate very limited impact on the planet, but the perception among the ill-informed is absolutely the opposite.

Consequently, numerous dormant assets are situated in marinas or ports globally, undergoing maintenance and preparation for the occasional owner visit. Compared to the private jet industry, we differ significantly. Yet a discernible trend emerges, one we expect to define our future.

To make our industry more investible and stable, we have to explore how we can make these floating assets work harder and not sit idle in various berths around the world. Just as private jets have become expensive to own and have garnered a stigma of excess when used for short domestic flights with only a few passengers on board, we anticipate a comparable trend within our industry.

More next-generation owners may realise that owning an asset 100 per cent for only 10 per cent of the year raises pertinent questions that could destabilise the market. Although superyachts are traditionally used in conventional summer and winter locations during favourable weather conditions, trends are shifting and new regions are emerging – extending the yachting season to 10 months. However, few owners can utilise their superyacht for such an extended period.

If owners or investors were presented with an alternative scenario, where a superyacht could be used for 75 per cent of the year, accommodating multiple users, owners or guests who pay for specific times on board, this could lead to significant transformations in our industry. The potential shift may involve more assets entering fleet ownership or business models focused on increased activity, revenues and access through fractional ownership, charter models and co-ownership programmes.

Such approaches could prove more logical and astute for buyers who recognise that the traditional capital expenditure versus operating expenditure equation is no longer sustainable in the future.

What lies ahead for ownership?

In essence, the future is promising. Over the short term (the next five years), we anticipate a continuation of current trends, with more buyers stepping forward to secure various assets and build slots. There are minimal indications of the market slowing down or demand decreasing. However, we must consider geopolitical factors, dramatic climate shifts, wealth inequality and alternative investments, lifestyles and appealing opportunities that might attract our customers.

Geopolitics: On a daily basis, scenarios worldwide impact various financial markets, encompassing events such as the Russian-Ukrainian war, Chinese economic stability, tensions in the South China Sea, raw-material demands across manufacturing sectors and efforts to control supply chains. Oil prices and the push for alternative energy sources add further complexities. Political landscapes see the rise of protests and demonstrations against energy-intensive projects. These developments make headlines and can result in financial instability.

Dramatic climate shifts: Annual discussions highlight the impact of climate change on our lives. This summer, the Mediterranean experienced heatwaves and unpredictable weather patterns. Severe climate events elsewhere in the world draw attention from governments and activists. If regional governments enforce restrictions on energy-intensive asset-cruising patterns, it might limit and further regulate future cruising destinations.

Wealth inequality: A few years ago at Davos, Oxfam delivered a significant report addressing wealth inequality. This issue drew the attention of global leaders, suggesting that addressing the world’s top one per cent is crucial to solving various global problems. As discussions around this topic gain traction, our customer base could become a target for taxation or negative media coverage. Consequently, UHNWIs might reconsider their lifestyle and profile.

Obviously, it’s not all doom and gloom. There’s a very simple opportunity to protect, defend and grow our industry by making sure every owner and potential owner understands the responsibility of having a high-profile floating asset in order to ensure that the media, negative observers, governments and the various NGOs fully understand the value and contribution of superyachts.

Today, no one makes money out of owning a superyacht and they generate very limited impact on the planet, but the perception among the ill-informed is absolutely the opposite. By shifting the narrative, changing asset-usage practices and demonstrating that superyachts can deliver positive impacts on the ocean and our planet, the future of ownership could become one of the most significant investments an UHNWI can make.

Investing in technology, research and development, science, philanthropy, design, engineering, manufacturing, future fuels, energy and new materials all contribute to the contemporary intelligent investor landscape.

If owners, buyers and investors are inspired to adopt the same principles through their next superyacht, our industry’s image can be transformed, and these stakeholders might generate more positive impacts on their investments by reducing their asset’s environmental footprint. Perhaps the focus should shift from superyacht ownership to investing in the future and utilising new superyachts as platforms for change.

This article first appeared in The Superyacht Owner Report. To gain access to The Superyacht Group’s full suite of content, publications, events and services, click here to join The Superyacht Group Community and become one of our members.

NEW: Sign up for SuperyachtNewsweek!

Get the latest weekly news, in-depth reports, intelligence, and strategic insights, delivered directly from The Superyacht Group's editors and market analysts.

Stay at the forefront of the superyacht industry with SuperyachtNewsweek

Click here to become part of The Superyacht Group community, and join us in our mission to make this industry accessible to all, and prosperous for the long-term. We are offering access to the superyacht industry’s most comprehensive and longstanding archive of business-critical information, as well as a comprehensive, real-time superyacht fleet database, for just £10 per month, because we are One Industry with One Mission. Sign up here.

Related news

Out Now: The Superyacht Owner Report

Issue 218: The Superyacht Owner Report is now available to read and download online

Owner

Mounting pressure to tax ‘hidden assets’ in the Balearics

A proposed tax on luxury assets in the Balearics could have a major impact on the superyacht industry

Owner

2023 - turbulent or exciting?

While global economic forecasts for 2023 may be uninspiring, emerging markets offer a new hope to the yachting industry

Opinion

Related news

Out Now: The Superyacht Owner Report

3 years ago

2023 - turbulent or exciting?

4 years ago

NEW: Sign up for

SuperyachtNewsweek!

Get the latest weekly news, in-depth reports, intelligence, and strategic insights, delivered directly from The Superyacht Group's editors and market analysts.

Stay at the forefront of the superyacht industry with SuperyachtNewsweek