Disrupt or be disrupted

Hot off the press from METS, Prof. Dr Christoph Ph. Schließmann comments on the new paridigm facing the superyacht industry…

Our regular guest contributor examines why the maritime industry has reached a strategic inflection point – and why the superyacht sector must redefine its own logic.

When Metstrade 2025 opened on 18 November in Amsterdam, one message cut through the noise: the maritime industry is not simply facing change, it is already deep inside a structural transformation. Frank Hugelmeyer, CEO of the National Marine Manufacturers Association (NMMA), set the tone with unusual clarity: “Change is coming. Disrupt or be disrupted.”

These words were not a cliché. They captured a profound shift impacting every layer of the maritime value chain – from entry-level leisure boats to the 54-billion-euro superyacht ecosystem. And the keynote that followed, delivered by Le Boat’s Managing Director Cheryl Brown, underscored the same truth: a new generation of consumers, new technologies and a new informational logic are rewriting the industry.

This article examines why leisure marine and the superyacht sector are simultaneously converging, diverging and exerting new influence on one another – and why the coming decade will demand a fundamentally different understanding of markets, customers, business models and lifecycle value.

Split waters: two industries, two logics, one strategic pressure

The recreational boating market is navigating what Hugelmeyer called “incredible economic uncertainty”. Consumer behaviour is evolving rapidly, discretionary spending is volatile and digital decision-making is accelerating.

The superyacht world, by contrast, is often described as a “€54 billion economic special zone” – a system that historically defies traditional market logic, where demand is often counter-cyclical and driven by asset security, privacy and mobility more than by macroeconomics.

But both markets now share one truth: they are being forced out of old paradigms and into a new strategic logic that is broader, more digital and far more complex.

Leisure marine: from product market to experience and algorithm economy

The leisure boating industry is no longer competing with other boat builders; it is competing with every sector fighting for consumer attention, time and emotional energy.

a) The customer journey becomes an AI-driven journey

Cheryl Brown captured it perfectly: Customers now “pop into ChatGPT and ask: ‘What’s the best boat holiday company?’” This means the first and most decisive battleground for demand is in algorithms, not brochures.

b) Ratings are the new currency

Trustpilot, Tripadvisor and Google reviews determine:

• Booking volumes

• Pricing power

• Brand reputation

• Competitive standing

• Visibility is no longer controlled by marketing budgets but by digital credibility.

c) ‘Simplify boating’ as a strategic imperative

New customers – especially post-pandemic – have:

• No boating background

• Little interest in ownership

• High expectations for seamless, guided, risk-free experiences

Le Boat’s strategy reflects this shift: 400 new boats (via Delphia/Groupe Beneteau), simplified UX, refined comfort concepts and AI-aware customer engagement.

A boat is no longer the core. The experience infrastructure around the boat is.

d) A platform replaces the product

The business model moves away from selling boats and towards:

• Charter and experience packages

• Subscription and access models

• Online platforms

• Partnerships with OEMs, marinas and tourism ecosystems

• A boat is no longer the core. The experience infrastructure around the boat is.

Superyachting: the quiet revolution inside a €54 billion system

The superyacht industry has long operated according to its own economic rules. But even this insulated sector is entering a period of strategic redefinition due to three forces:

• A younger, more dynamic UHNWI generation

• A professionalised, data-driven lifecycle model

• Intensifying regulatory, climate and insurance pressures

a) New build remains king but no longer the centre of gravity

The new-build market continues to grow, especially in the 30 to 40-metre range, but the most consequential shift is the rise of the lifecycle economy:

• Operation (crew, compliance, digital management)

• Refit and upgrade cycles (a €2.3bn driver with stable long-term demand)

• Brokerage and charter intermediaries (increasingly digital and globalised)

In this new model, value is not linear, it is circular.

b) Flexible ownership models are entering the mainstream

Fractional structures, multi-vessel access programmes and hybrid ownership/charter models are rapidly gaining relevance.

For the younger wealth cohort, a superyacht is:

• A service platform

• A mobile lifestyle asset

• A customisable personal space

– not a static monument.

c) Insurance and climate risk are rewriting the economics

The industry faces:

• Rising premiums

• Reduced insurer appetite in high-risk regions

• More exclusions (especially storm-related)

• Operational constraints shaped by climate modelling

• Risk has become a strategic design parameter, not an operational afterthought.

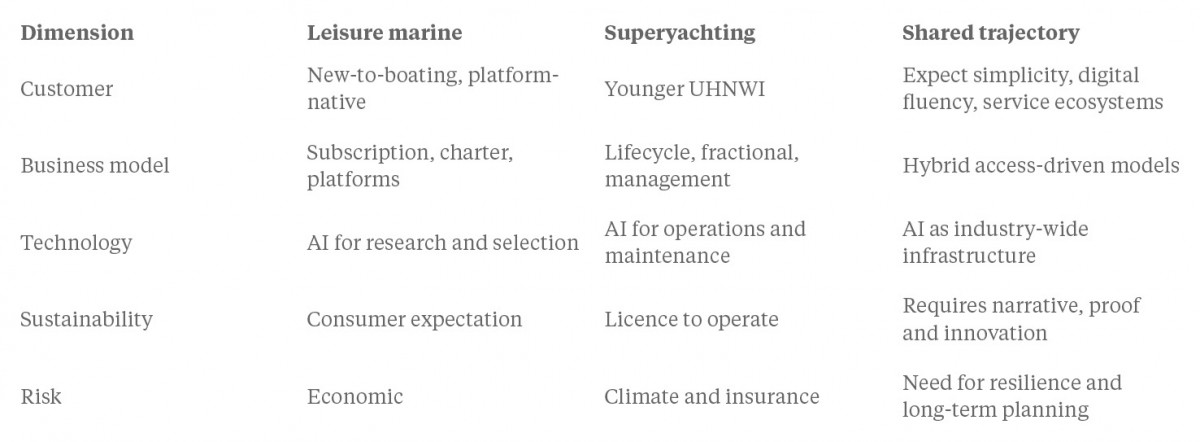

d) The new interdependence: why both markets are linked

Although vastly different in scale and clientele, leisure marine and superyachting are now connected by structural parallels:

The strategic thesis: the maritime industry enters the age of system strategy

Both markets are transitioning from product-centric to system-centric logic.

a) Access beats ownership

Demand shifts toward flexibility over control.

b) Data becomes more important than tradition

Decisions are driven by:

• Reviews

• Algorithms

• Lifecycle performance data

• Transparency in service histories

c) Lifecycle value is the new profit engine

Controlling the full cycle (new build → operation → refit → re-sale) becomes the sector’s most powerful competitive advantage.

d) Customers are becoming co-architects

They expect:

• Personalisation

• Immediacy

• Digital management

• Sustainability

• Seamless experience chains

e) Boundaries between sectors dissolve

Both industries compete not for product share but for:

• Emotional relevance

• Time

• Autonomy

• Experiential superiority

The superyacht industry, despite its strength, is at a paradoxical moment:

economically resilient, strategically exposed.

What the superyacht industry must do now

a) Redefine the Strategic Relevant Market (SRM)

It is no longer “superyachts” but:

• Experience assets

• Mobile private spaces

• Security and autonomy platforms

• Multimodal lifestyle systems

b) Master the lifecycle economy

Shipyards, managers and operators must:

• Secure data ownership

• Integrate operation, refit and upgrade pathways

• Build digital service layers

• Close the loop between build → use → renewal

c) Align with the new UHNWI mindset

Younger buyers want:

• Speed

• Transparency

• Personalisation

• Digital interfaces

• Flexible usage models

d) Treat AI as infrastructure, not innovation

Including:

• Predictive maintenance

• Digital twins

• Automated compliance

• AI-assisted crew management

e) Craft a credible sustainability and legitimacy narrative

Not as compliance but as strategic storytelling and industry positioning.

Conclusion: the future belongs to those who redraw the map

Metstrade 2025 made one thing clear: the maritime industry has entered a decade in which product, market and customer logic are being redesigned simultaneously.

The superyacht industry, despite its strength, is at a paradoxical moment: economically resilient, strategically exposed. “Disrupt or be disrupted” is not a warning. It’s an accurate description of a moment in which technology, customer expectations and lifecycle economics are rewriting the rules.

The winners of the next decade will be those who understand:

• A yacht is no longer an object.

• It is a system.

• An experience.

• A platform.

• And a strategic asset for the future.

As an open-source platform we offer an industry-wide invitation to anyone and everyone in our sector to share their knowledge, experience and opinions. So if you have an interesting and valuable contribution to make, and would like to join our growing community of guest columnists, share your ideas with us at newsdesk@thesuperyachtgroup.com

NEW: Sign up for SuperyachtNewsweek!

Get the latest weekly news, in-depth reports, intelligence, and strategic insights, delivered directly from The Superyacht Group's editors and market analysts.

Stay at the forefront of the superyacht industry with SuperyachtNewsweek

Click here to become part of The Superyacht Group community, and join us in our mission to make this industry accessible to all, and prosperous for the long-term. We are offering access to the superyacht industry’s most comprehensive and longstanding archive of business-critical information, as well as a comprehensive, real-time superyacht fleet database, for just £10 per month, because we are One Industry with One Mission. Sign up here.

Related news

The silent threat on the water

Sarah Willis, founder of digital-privacy and online-reputation consultancy SABLR, spells out how AI is rewriting risk for superyacht owners

Owner

Metstrade 2025: the only place that matters

If you’re not at the RAI from 18 to 20 November, what are you even doing? Amsterdam awaits the industry’s most valuable gathering

Event

Charter – it’s more than just about looks …

The golden rules to optimise charter income from a superyacht while still protecting the owner’s valuable asset

Opinion

Drawing the line between commercial and private use

Substance over weekends: private use inside commercial yacht structures is the EU-compliance frontier

Opinion

Related news

The silent threat on the water

8 months ago

Metstrade 2025: the only place that matters

9 months ago

Charter – it’s more than just about looks …

9 months ago

Drawing the line between commercial and private use

9 months ago

NEW: Sign up for

SuperyachtNewsweek!

Get the latest weekly news, in-depth reports, intelligence, and strategic insights, delivered directly from The Superyacht Group's editors and market analysts.

Stay at the forefront of the superyacht industry with SuperyachtNewsweek