Securitised loans and their place in the superyacht industry

Credit Suisse has securitised a portfolio of superyacht and private jet loans, but what does this mean?

Credit Suisse has securitised a portfolio of superyacht and private jet loans, in order to offload some of the risks associated with high value lending to UHNW individuals through an innovative, synthetic SRT (significant risk transfer) transaction for capital and balance sheet management purposes. But what does this really mean?

Effectively, Credit Suisse securitised the risk of these loans, currently valued at $2bn notional value, provided to their UHNW clients. The high value loans are collateralised by their yachts, jets and other high value financial assets such as real estate. One of the key things to mention is that the securitisation of loans is a perfectly normal banking technique, that is often done using mortgage portfolios and other valued assets to back up the potential risks of high value loans.

What makes the news about Credit Suisse unique is that the use of yachts and private jets to back the deal is believed to be a market first for a private bank, such as Credit Suisse. Of this $2bn, $80m was securitised, which means that Credit Suisse offloaded the first loss of the portfolio up to this value to asset management companies and hedge funds, who are now the ones who would be liable if the borrowers who took out the loan defaults. It is worth mentioning that by the synthetic nature of the transaction, the buyers of the first loss protection do not have visibility over individual borrowers, as they write a portfolio guarantee which is priced based on aggregated portfolio expected default statistics. From the banks perspective, synthetic securitisation frees up Risk Weighted Assets (RWA), which in turn, improves the economic return on the portfolio of interest. This allows for Credit Suisse the ability to reinvest more risk capacity into future lending deals. In short, the transaction allows Credit Suisse the capacity to keep lending to more clients, expanding its portfolio further.

Some have speculated that the growing conflict between Russia and Ukraine and potential sanctions from western countries could be a future driving factor in the need to protect lenders from external factors causing borrowers to default on loans. For further context, Credit Suisse previously experienced twelve loan defaults on both aircraft and yacht loans during 2017 and 2018, which was believed to be due to US sanctions introduced against Russian oligarchs during the Trump administration. However, one should note that this transaction already closed in November 2021 prior to the escalation of the Ukrainian conflict in December and, therefore, it is unlikely that Credit Suisse intentionally entered into this transaction as a hedge for the following Ukraine crisis.

Financing yacht loans is not a new concept. There are typically two routes that a potential owner can go down if they are wishing to purchase a superyacht. Like buying a house, most second hand buyers will take out a ‘yacht mortgage’ on the vessel they are interested in. However, there are many factors which feed into this process, known as a Loan-to-Value (LTV) assessment, such as; who built the yacht, where will the vessel be registered, taxation of the yacht, whether it will be used privately and/or commercially and the potential owner’s tax status and history. Most yacht loans are arranged in a way where the ‘yacht mortgage’ is protected against any other potential creditor claims attributed to the borrower.

The other type of yacht financing is a ‘yacht-building loan’ or ‘yacht-construction loan’. This type of financing is complex and normally is an agreement between the owner and the bank, where the bank will pay lump sums when the new build process reaches key milestones, such as laying a keel and when a vessel is at sea trials and the potential owner will make payments towards those lump sums. Up until the delivery of the vessel, the bank is the technical owner of the yacht, meaning that if there is a default in payments, the bank can contract the shipyard to finish the build process and sell to a new owner or can find a new owner to take over the build process and take up where the payments left off.

Yacht loans are crucial for the superyacht industry as ‘yacht mortgages’ keep the second-hand brokerage market turning over by allowing potential owners access to the upfront cash to commission newly constructed yachts and buyers to purchase brokerage vessels. These agreements help keep the superyacht market buoyant. This allows for the growth of the superyacht fleet, which allows for the growth of the entire superyacht ecosystem to grow further, stretching from the craftsmen who build the vessel to the provisioners who supply goods on board.

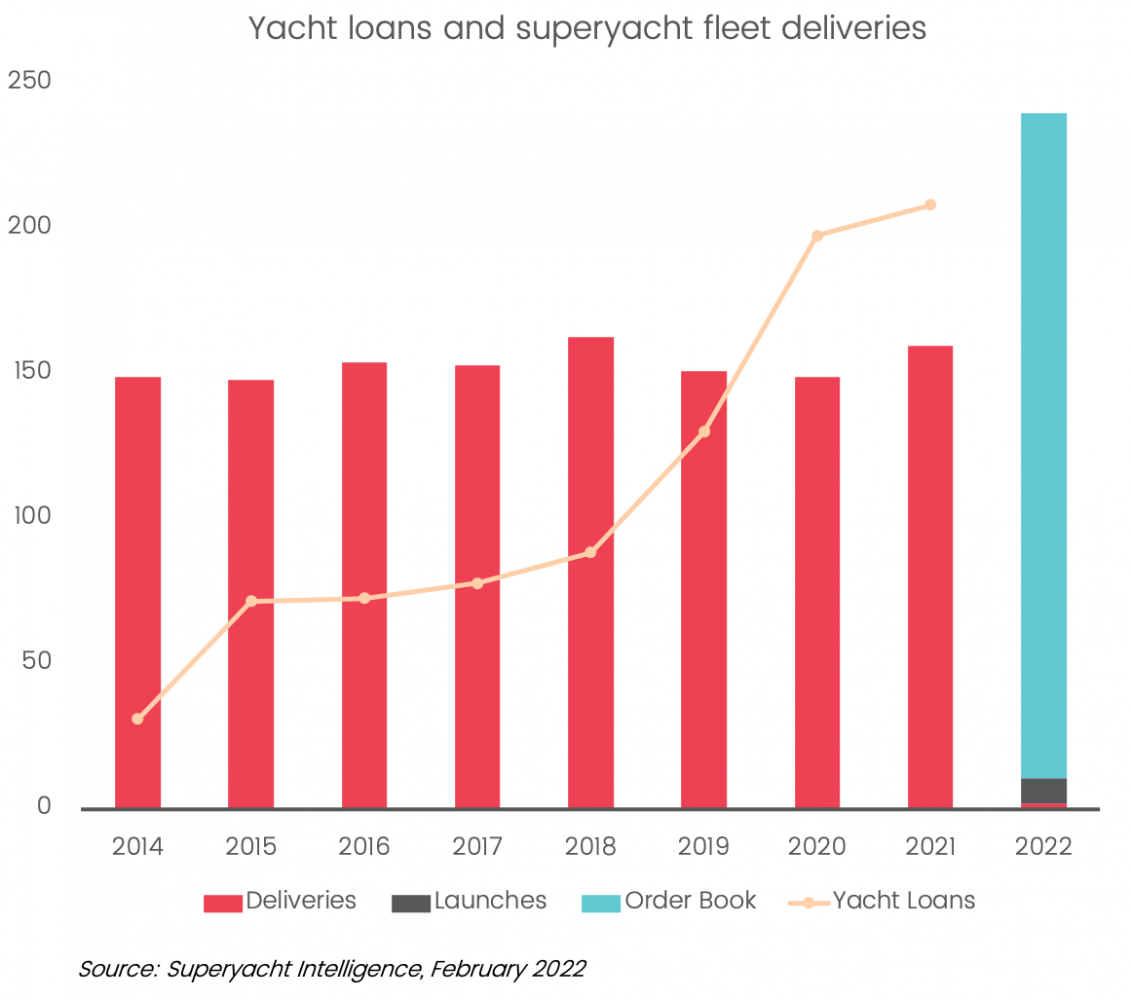

The above graph shows how yacht loans from Credit Suisse has increased since 2014 and in 2021 were valued at over $1bn. Credit Suisse is one of many institutions that provide capital for yacht loans, therefore, this trend line is merely meant to represent how the value of yacht loans is increasing year on year. When overlaid with the superyacht fleet and the current order book for 2022, it demonstrates how the increase in yacht loans has helped to contribute to the fleet growth, in particular with 240 vessels projected to be delivered throughout 2022, correlating to the fairly sharp increase in yacht loans seen between 2018 and 2020, when most of those contracts would have been taken out with the various shipyards.

Yacht finance is crucial in the superyacht industry, allowing more potential owners to access the market both through new build and second-hand sales. As the UHNW population grows, so does the pool of potential owners who may take out this type of finance option with institutions such as Credit Suisse, however, with the unforeseen circumstances such as geo-political situations and pandemics to contend with in the last couple of years, as well as potential data leaks in the ever expanding digital age, it is completely understandable why these institutions would look towards utilising strategies that help protect them.

Profile links

NEW: Sign up for SuperyachtNewsweek!

Get the latest weekly news, in-depth reports, intelligence, and strategic insights, delivered directly from The Superyacht Group's editors and market analysts.

Stay at the forefront of the superyacht industry with SuperyachtNewsweek

Click here to become part of The Superyacht Group community, and join us in our mission to make this industry accessible to all, and prosperous for the long-term. We are offering access to the superyacht industry’s most comprehensive and longstanding archive of business-critical information, as well as a comprehensive, real-time superyacht fleet database, for just £10 per month, because we are One Industry with One Mission. Sign up here.

Related news

Giving back

We explore a report on UHNW philanthropy and consider what this means for the superyacht market

Owner

The fleet forecast

We provide a snapshot of superyacht delivery figures for the next five years using three forecasting models

Fleet

Sanlorenzo superyacht division revenues reach €133.2M

Superyacht revenues are up by 33.5% on the previous period and account for 31.1% of all Sanlorenzo yacht sales

Business

Managing glamorous money

Jane Turner, CEO of fintech company Centtrip, discusses money management in the superyacht industry

Crew

Combining brokerage and financing

The team at Compleo Superyachts discusses the benefits of combining financing and brokerage

Business

Related news

Giving back

5 years ago

The fleet forecast

5 years ago

Managing glamorous money

5 years ago

Combining brokerage and financing

5 years ago

NEW: Sign up for

SuperyachtNewsweek!

Get the latest weekly news, in-depth reports, intelligence, and strategic insights, delivered directly from The Superyacht Group's editors and market analysts.

Stay at the forefront of the superyacht industry with SuperyachtNewsweek