Which shipyards are most consistent?

The Superyacht Agency has explored the shipyard dynamics of the last 30 years…

Since 1990, the superyacht fleet has quadrupled in size; currently sitting at 5,568 vessels, there is no question that the superyacht landscape is a very different to how it was 30 years ago. Acting as the market’s most reliable barometer, The Superyacht Agency has explored the shipyard dynamics of the last 30 years, illustrating where we are as an industry, its evolution and what we can expect in years to come.

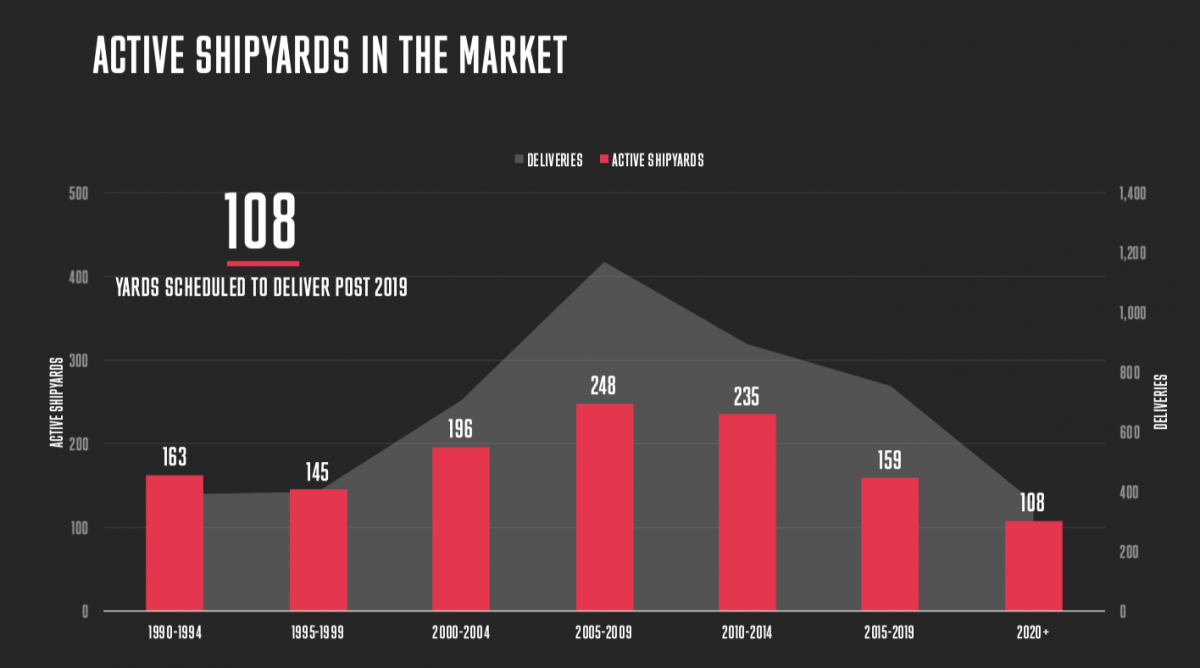

As consistency is important to the health of the new build market, it is important to understand the changing ratio of the number to deliveries to the number of active shipyards. Between 1990 and 1994, there were 163 active shipyards that collectively delivered 386 vessels within this period, which equates to 2.37 superyachts delivered per shipyard. Between 2005 and 2009 there was a surge in the number of active shipyards to 248, which collectively delivered 1171 vessels, equating to 4.72 deliveries per yard.

And, most recently, it appears we have witnessed the completion of a market adjustment. Between 2015 and 2019, there have been 159 active shipyards recorded (returning to the levels of the 90s), which together have delivered a total of 752 superyachts, equating to 4.73 vessels per shipyard. This is almost exactly the same figure as the boom period of the mid-2000s. As the figures suggest, the market has achieved a degree of equilibrium, and output per shipyard is its highest ever. But it hasn’t always been this way.

The global financial crisis (GFC) left an indelible mark on the superyacht industry, when the market peaked and 266 superyachts were delivered. Over this period, keeping output consistent was a serious challenge, as the GFC was responsible for the demise of a number of shipyards, causing a trough of delivery figures in 2015, following a steady decline.

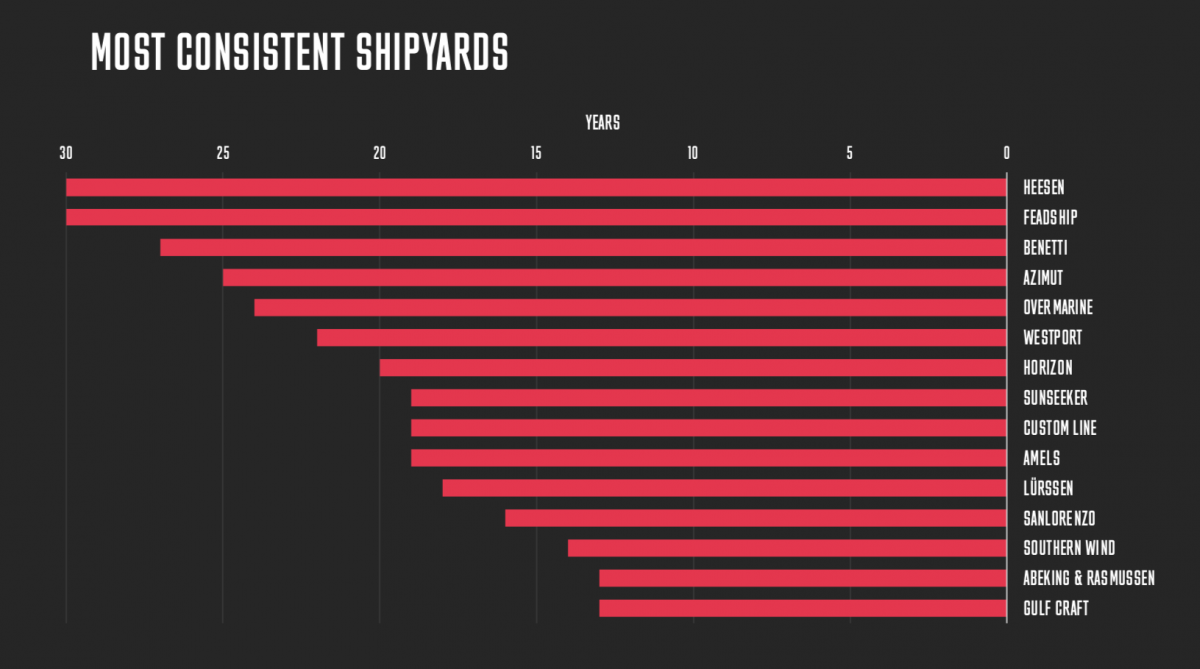

There are 15 shipyards that really stand out when it comes to consistency, the most prominent being Dutch superyacht builders Heesen and Feadship, both of which have made at least one delivery every year for at least the last 30 years. In fact, Heesen and Feadship have made a monumental contribution to global superyacht activity over the last 30 years, collectively delivering 43.7 per cent of the Dutch superyacht fleet in unitary terms.

In the Netherlands alone, there have been 38 active shipyards in the last 30 years, but the five most active shipyards (Heesen, Feadship, Amels, Royal Huisman and Oceanco) account for 67.3 per cent of Dutch output over that time period, further pointing to the consolidation of the market among an elite tier of builders.

When it comes to shipyard output, a small collective of five shipyards have dominated unitary output over the last three decades; Azimut, Benetti, Sanlorenzo, Sunseeker and Westport have delivered 18.2 per cent of the entire fleet within this period.

The Superyacht Agency has identified that there are 108 shipyards with planed deliveries post 2019, 91 of which plan to make at least one delivery this year. Clearly, this period of consolidation and market adjustment endures, and it serves to highlight the work of the consistent shipyards who stand out through their impressive longevity.

Profile links

NEW: Sign up for SuperyachtNewsweek!

Get the latest weekly news, in-depth reports, intelligence, and strategic insights, delivered directly from The Superyacht Group's editors and market analysts.

Stay at the forefront of the superyacht industry with SuperyachtNewsweek

Click here to become part of The Superyacht Group community, and join us in our mission to make this industry accessible to all, and prosperous for the long-term. We are offering access to the superyacht industry’s most comprehensive and longstanding archive of business-critical information, as well as a comprehensive, real-time superyacht fleet database, for just £10 per month, because we are One Industry with One Mission. Sign up here.

NEW: Sign up for

SuperyachtNewsweek!

Get the latest weekly news, in-depth reports, intelligence, and strategic insights, delivered directly from The Superyacht Group's editors and market analysts.

Stay at the forefront of the superyacht industry with SuperyachtNewsweek