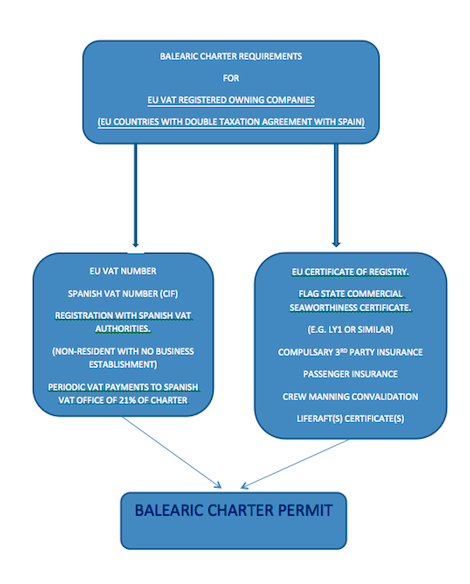

Finally, some welcome clarification

Following pressure from the ascoiación nacional de empresas nåuticas, the Spanish Directorate-General of Taxes has issued concrete clarification about the terms under which non-Spanish residents can operate commercially. The parameters have been welcomed by the industry.…

Upon receiving a response, anen issued the following statement:

Both the beneficial owner of a yacht and the persons related to that owner can use the yacht while taking the exemption provided [that the yacht is] actually and exclusively used for sailing charter activities (art. 66.1.g) of Law 38/1992, on Special Taxes): (i) in all cases, where the yacht is used outside Spanish territorial waters, because the legislation on special taxes may only be construed to apply within the territorial scope of that tax, which is Spain, and, (ii) in Spanish territorial waters, provided the beneficial owner or the persons related to the beneficial owner are not resident in Spain and do not have an “establishment” situated in Spain.

This news follows confirmation from the Spanish Directorate-General of Taxes (DGT) that, ‘the taxable event for the matriculation tax is the registration in Spain or sailing and use in Spain, of a yacht by persons or entities resident in Spain or owners of establishments situated in Spain. As a result, the sailing and use of a yacht outside Spain will not trigger the taxable event and therefore the tax will not be chargeable.’

And with regards the use of the yacht in Spanish waters by owners who are not resident in Spain, DGT ruled that, ‘the fact that the yacht is licensed to be chartered to persons or entities related to the charterer, where those persons or entities are not resident in Spain and do not own establishments situated in Spain, does not change the circumstances determining the requirements for exemption and therefore, does not trigger the tax.”

Commenting on this decision, Tax Marine’s Alex Chumillas said:

“This interpretation is a radical change compared with the previous situation, which did not allow a single use of the yacht by a related person or entity to the owning company. In those cases, where the related party is resident in Spain the limitation still applies. We do understand that to structure this use by the beneficial owner, there should be a charter agreement in place, and the charter fee should be agreed at arm’s length and VAT applied.”

The English translation of the official ruling, which has been provided by Tax Marine, is available to view here.

Profile links

NEW: Sign up for SuperyachtNewsweek!

Get the latest weekly news, in-depth reports, intelligence, and strategic insights, delivered directly from The Superyacht Group's editors and market analysts.

Stay at the forefront of the superyacht industry with SuperyachtNewsweek

Click here to become part of The Superyacht Group community, and join us in our mission to make this industry accessible to all, and prosperous for the long-term. We are offering access to the superyacht industry’s most comprehensive and longstanding archive of business-critical information, as well as a comprehensive, real-time superyacht fleet database, for just £10 per month, because we are One Industry with One Mission. Sign up here.

NEW: Sign up for

SuperyachtNewsweek!

Get the latest weekly news, in-depth reports, intelligence, and strategic insights, delivered directly from The Superyacht Group's editors and market analysts.

Stay at the forefront of the superyacht industry with SuperyachtNewsweek