Declining delivery figures. Says who?

While the 30-40m market struggles to recover, the 60m-plus market is now performing better than ever…

The lay conception is that the superyacht new build market is performing worse now than it did during the height of its pomp in the mid-to-late 2000s. As a general comment, this is accurate. In 2008, 266 30m-plus superyachts were delivered. By stark contrast, in 2018, only 146 superyachts were delivered. One may be forgiven, therefore, for assuming that this decline is representative of a decline in new build figures across the board. However, when one considers the various size sectors, an altogether different picture of the superyacht market emerges, with the 60m-plus market performing better now than it ever has done.

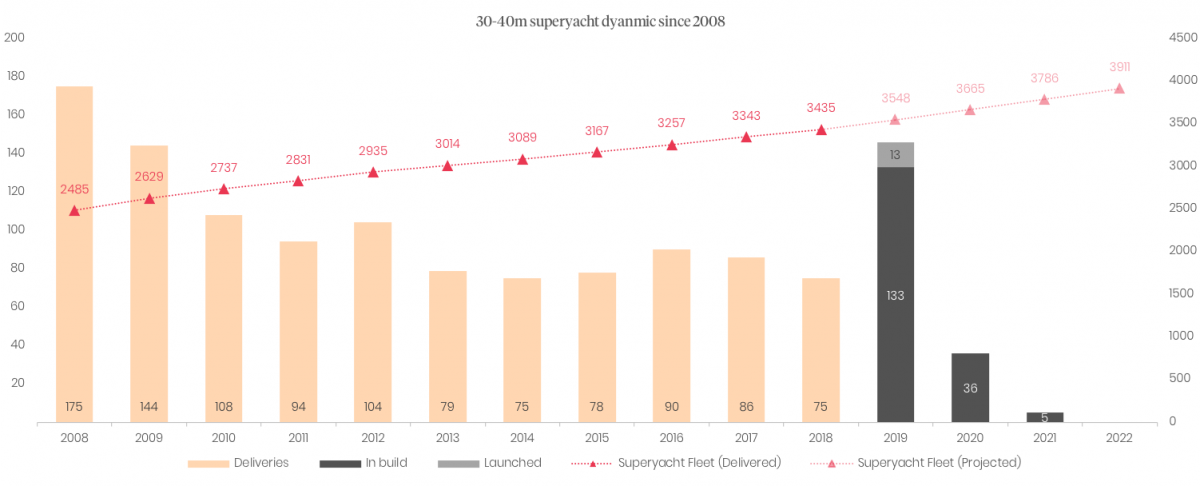

While the vast majority of the global fleet is still accounted for by vessels in the 30-40m range, with some 63.3 per cent of the fleet falling within this category, it is this size range that has suffered most in the post-global financial crisis (GFC) era. In 2008, 175 30-40m vessels were delivered. In 2018, there were 75 30-40m vessels delivered, less than half of the number in 2008. Exactly why this size range suffered such a dramatic collapse is open to interpretation, but it may have a lot to do with the fact that the owners who buy in this size range are more susceptible to global financial forces, in terms of personal wealth, and are more averse to conspicuous consumption in today’s economic climate.

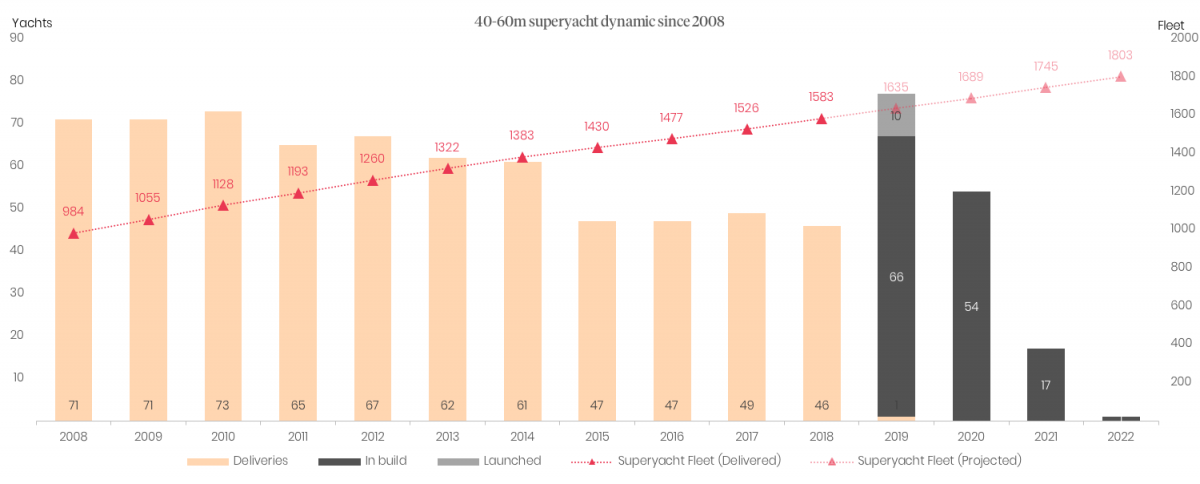

As the vessels grow in size, however, the post-GFC delivery collapse becomes less and less prominent. In 2008, there were 71 40-60m superyachts delivered compared to 46 vessels in this size range in 2018. Yes, the decrease in delivery figures is still significant. And yet, the decrease is less dramatic, in percentage terms, than that experienced by the 30-40m market.

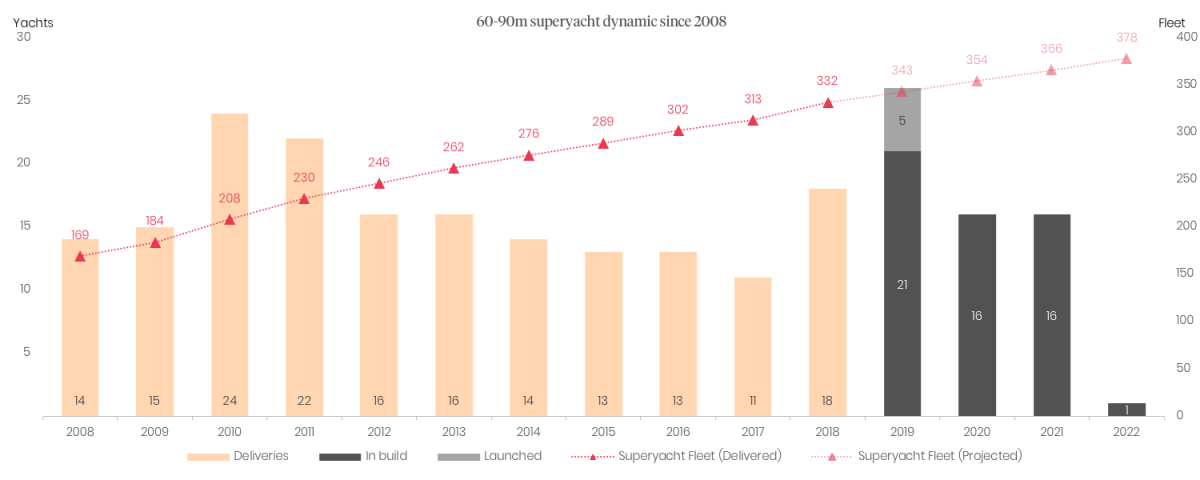

Importantly, once superyachts exceed 60m in length overall the post-GFC collapse is no longer evident. Indeed, the 60-90m size range has performed admirably since 2008, frequently matching, or exceeding, 2008’s 14 deliveries. On average, the 60-90m sector has delivered 16.2 vessels annually every year since 2008 and, if the order book proves to be accurate, a further 26 deliveries are due in 2019, making it the most prolific year to date.

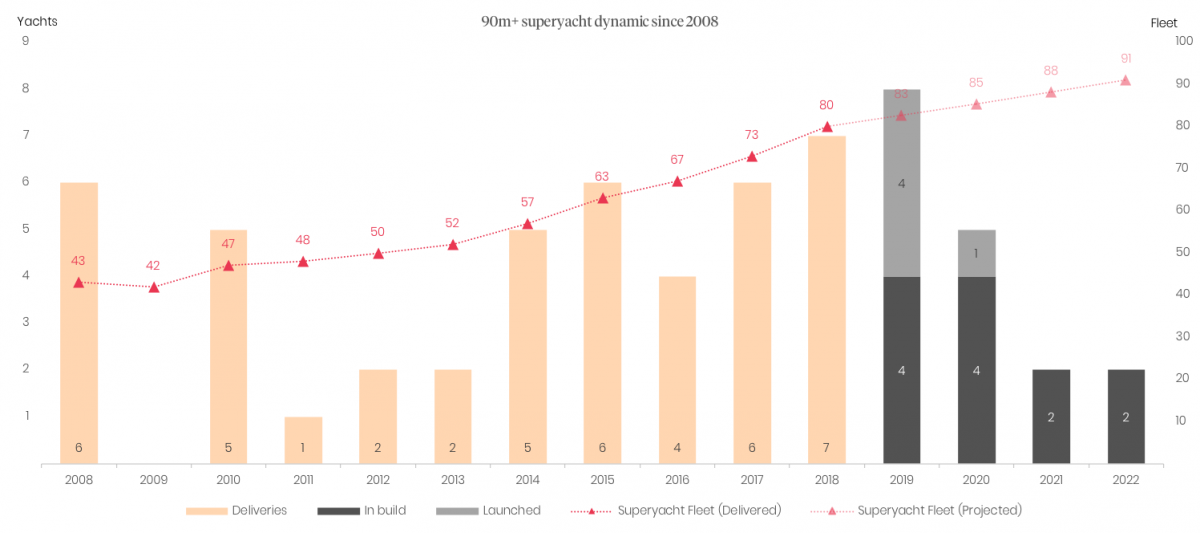

Relatively speaking, the 90m-plus market is a new one. In the past there were, of course, a number of large projects, with the most prolific years falling in 2005 and 2008, when there were five and six deliveries respectively. However, it is not until recent years that the 90m-plus sector has shown any signs of stability. During the period between 2000-2009, there was an average of two 90m-plus deliveries per year. During the following period from 2010 to the present day, there has been an average of 4.2 deliveries per year and within the last five years there has been an average of 5.6 deliveries per year. The 90m-plus market is now outperforming the period of yachting history that most consider to be the industry’s most productive period.

That the superyacht new build market is performing poorly is a misnomer. It can, at times, be useful to produce commentary on the superyacht market as a whole. But, in order to understand the nuances of the new build industry, it is imperative that analysis makes clear distinctions between the relative performances of the various size categories. In The Superyacht New Build Report, which is now available to purchase, we consider the performance of the new build sector using a variety of metrics that clearly highlight the direction that the market it moving in.

Click here to become part of The Superyacht Group community, and join us in our mission to make this industry accessible to all, and prosperous for the long-term. We are offering access to the superyacht industry’s most comprehensive and longstanding archive of business-critical information, as well as a comprehensive, real-time superyacht fleet database, for just £10 per month, because we are One Industry with One Mission. Sign up here.